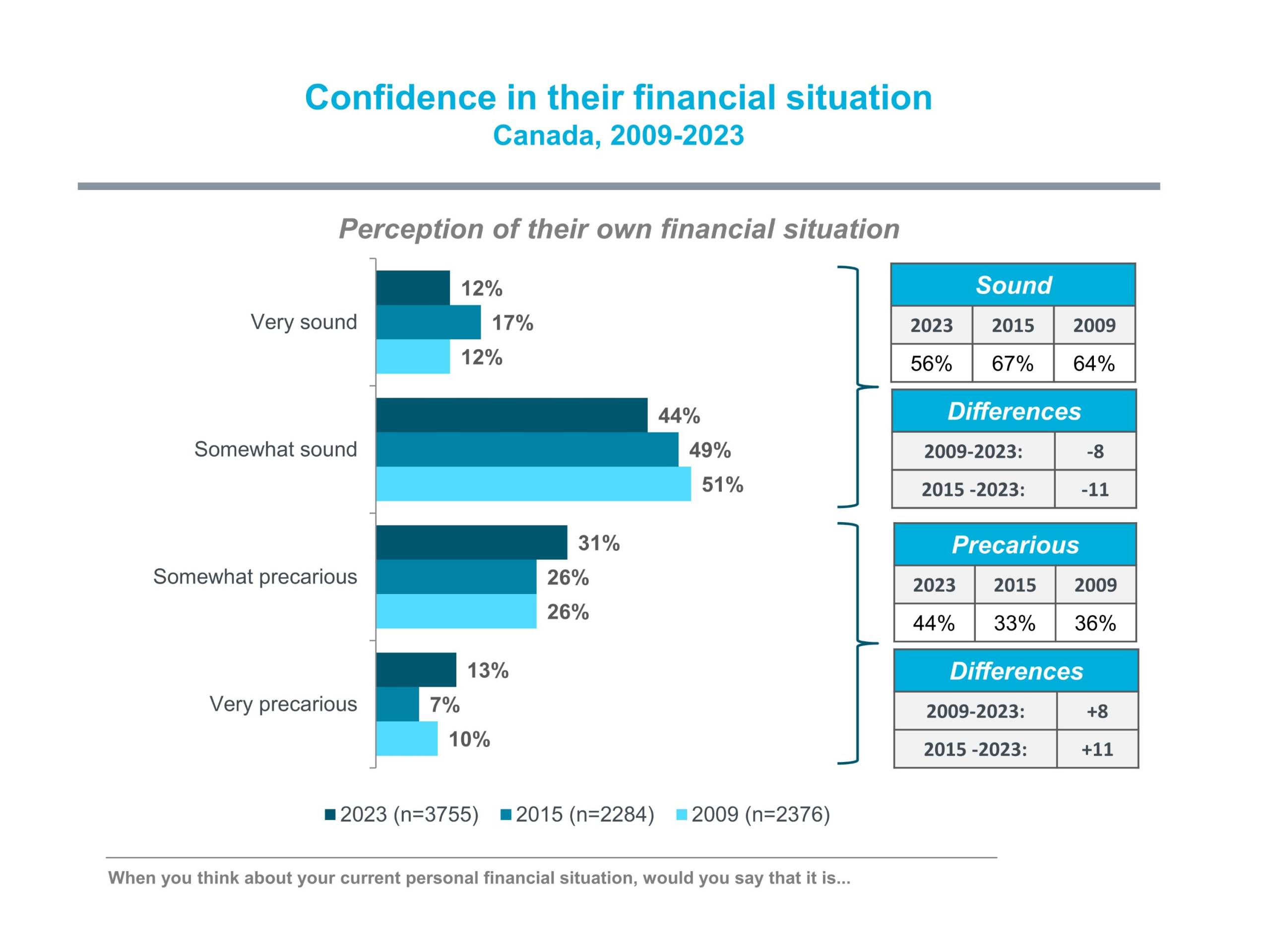

A loss of consumer confidence

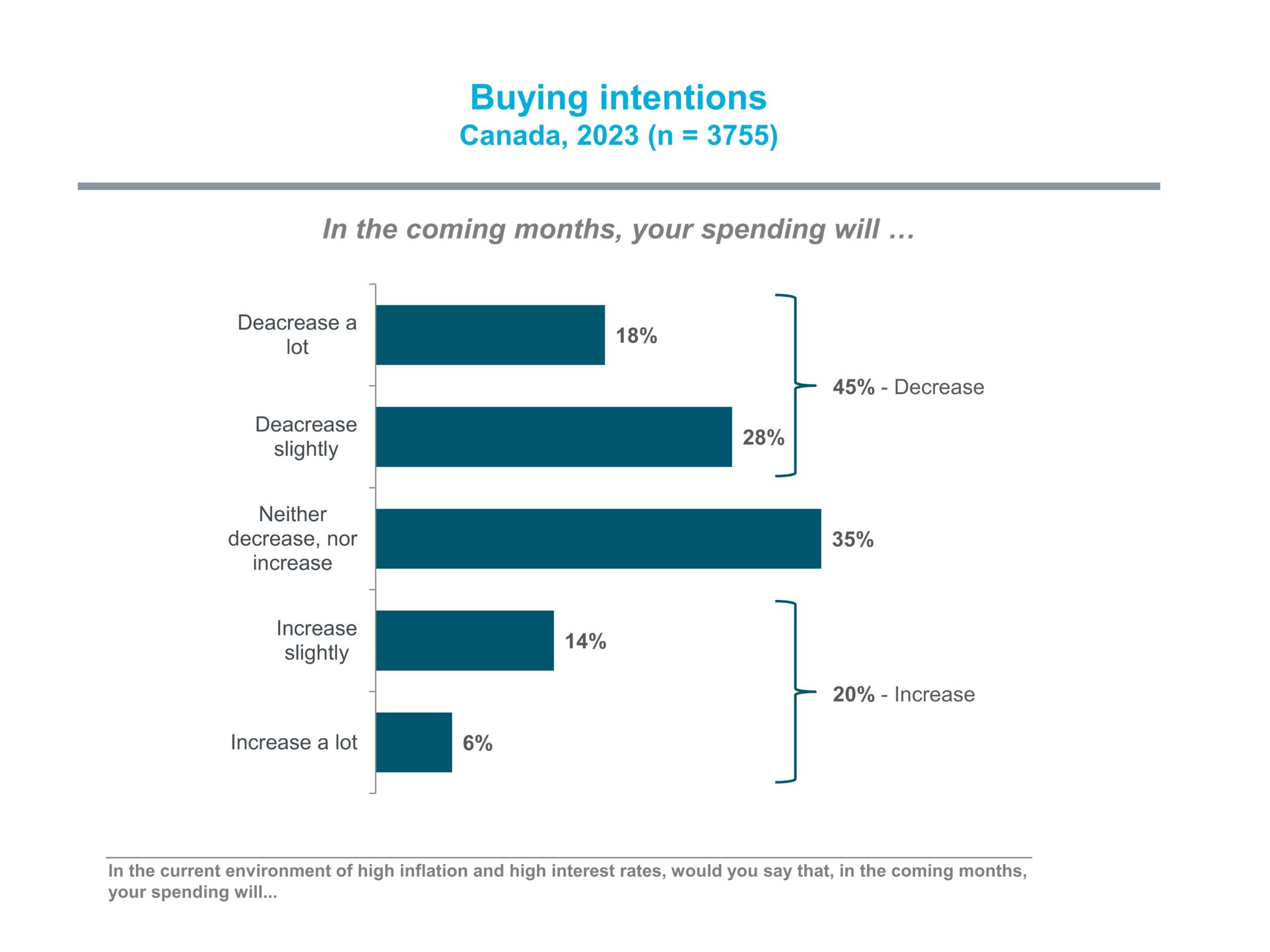

The future is looking darker!

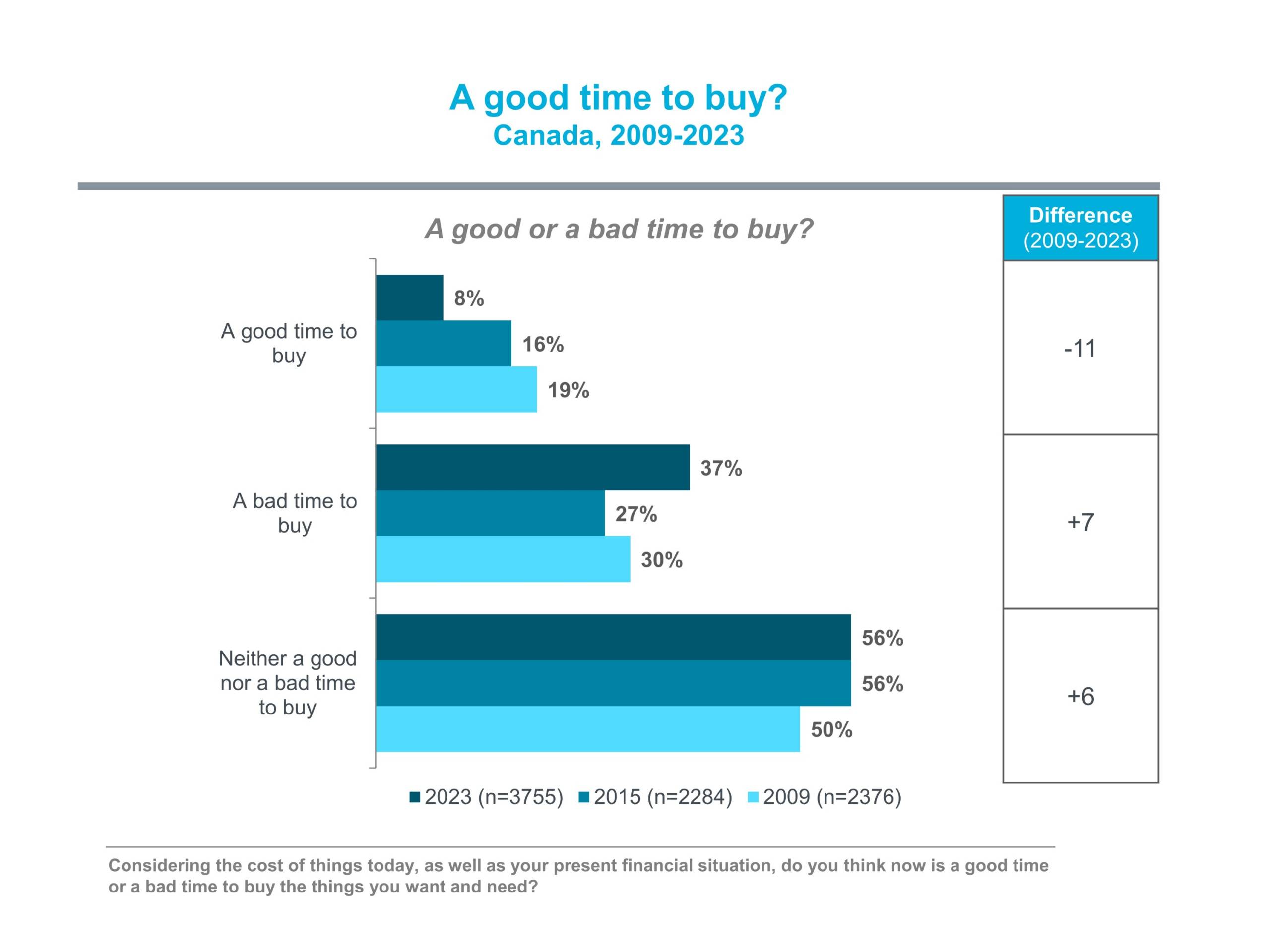

A good time to shop?

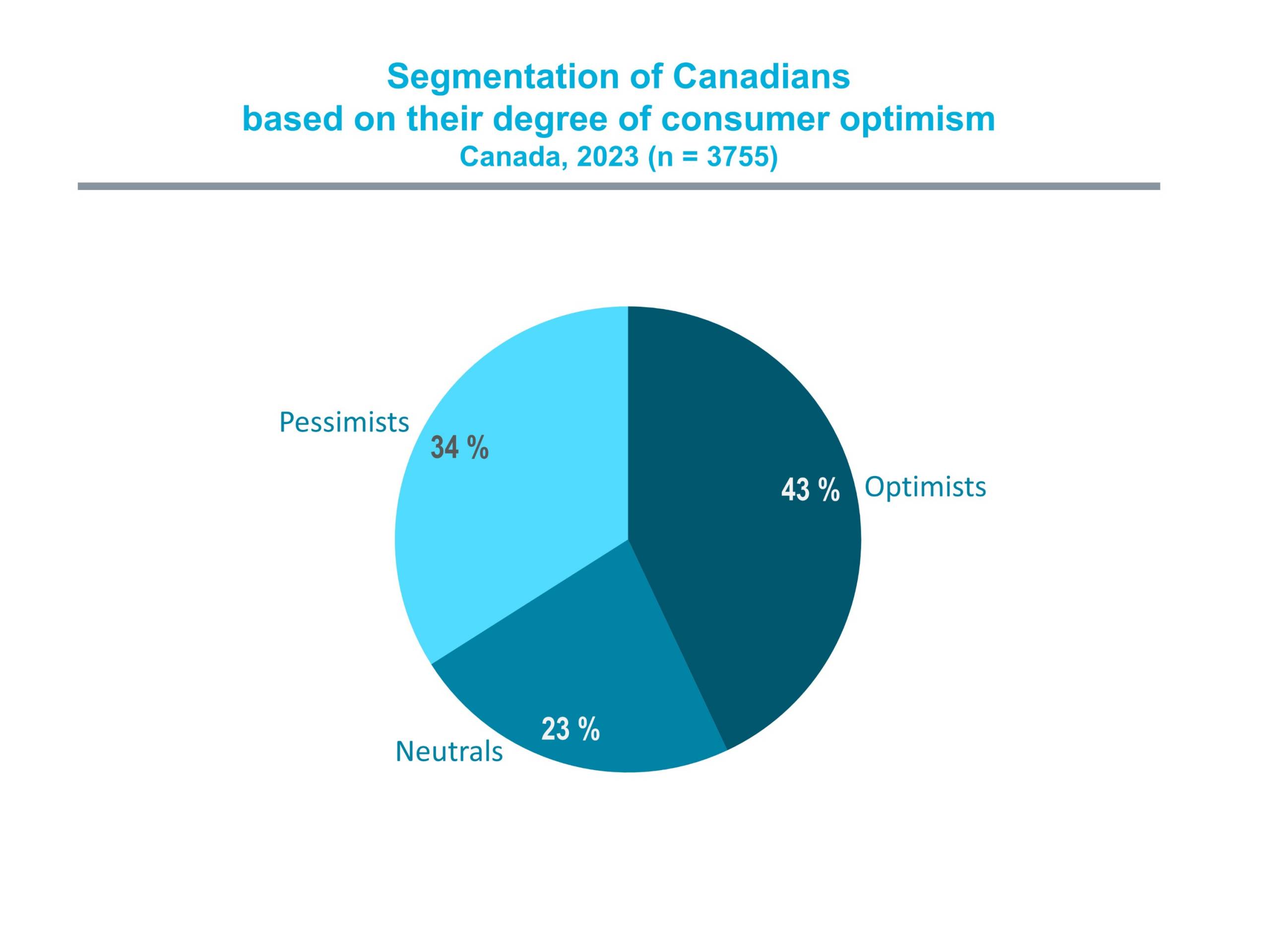

Many Canadians are still optimistic consumers

Optimists (43%)

Neutrals (23%)

Pessimists (34%)

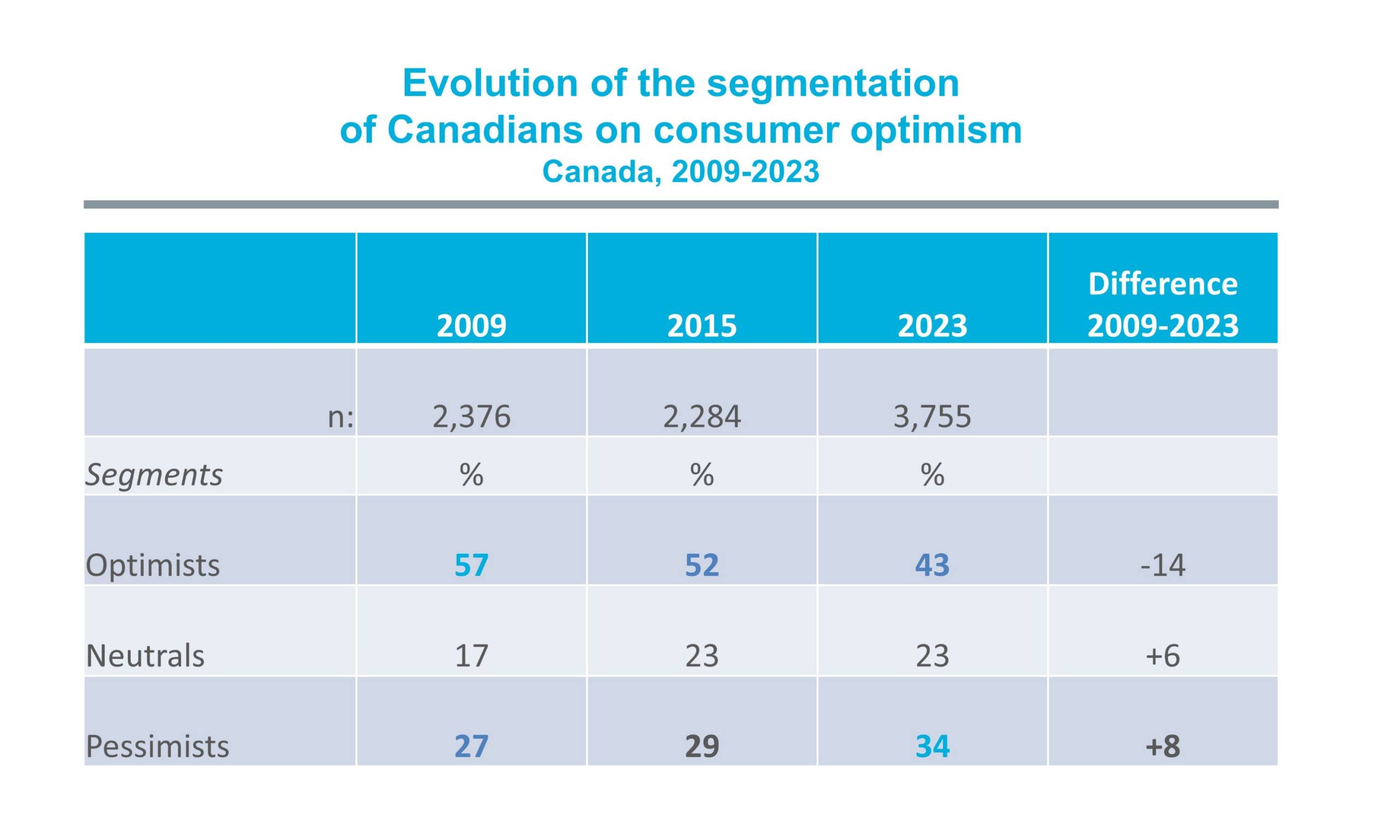

Trends in the evolution of this classification since 2009

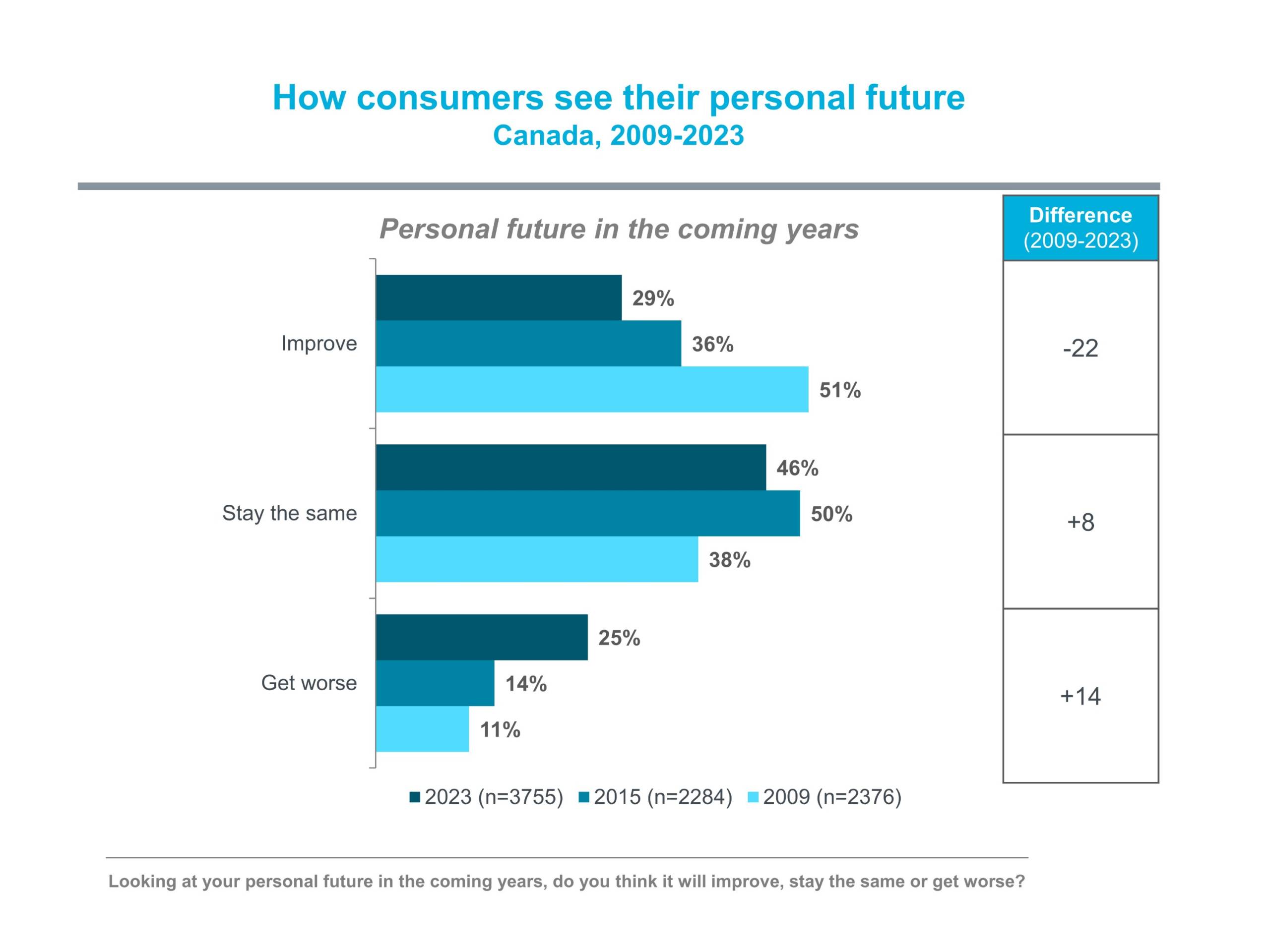

What to expect in the coming months/years